Because that page is basically screaming one thing:

the market just chose STRC as the main capital engine.

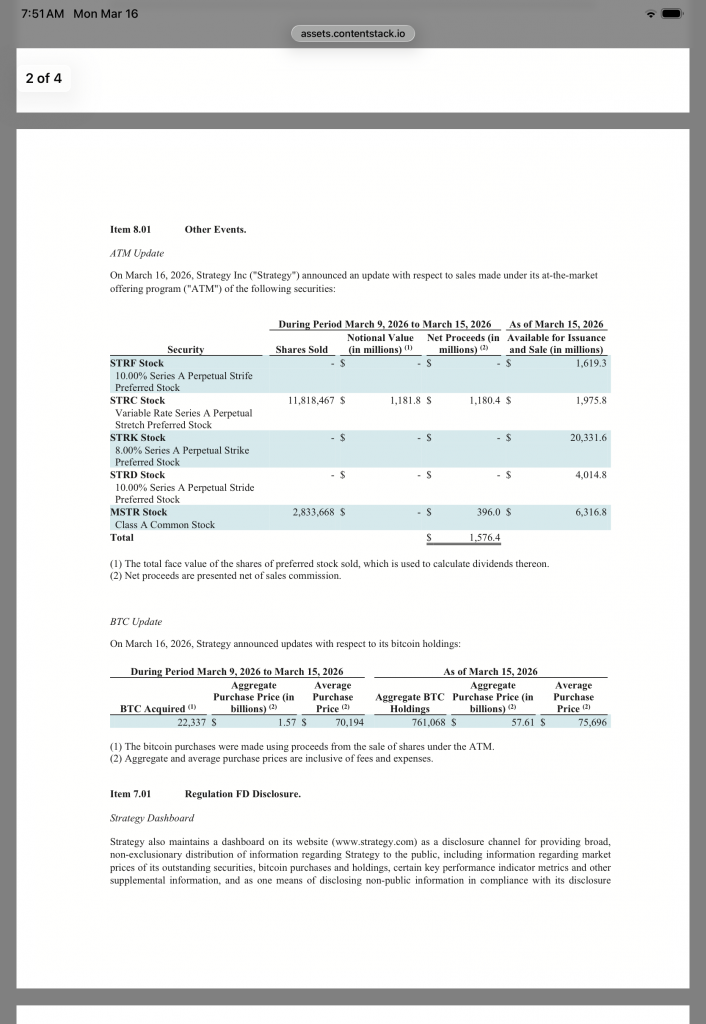

In the March 9–15 window, Strategy sold 11,818,467 STRC shares for $1.1818B notional and $1.1804B net proceeds. In the same filing, MSTR common only brought in $396.0M, while STRF, STRK, and STRD showed zero sales that week. That means roughly 74.9% of the entire week’s capital raise came from STRC alone. That is not “some demand.” That is a full-blown institutional vote.

Then the next punch lands: Strategy says the ATM proceeds were used to buy 22,337 BTC for about $1.57B, bringing total holdings to 761,068 BTC. So STRC is not just trading well in isolation — it is actively functioning as a giant conduit that turns yield demand into more bitcoin on the balance sheet.

Why this is extra savage for STRC specifically: STRC is designed to be Strategy’s short-duration, high-yield preferred, currently paying 11.50% annual dividends, monthly in cash, with the dividend rate adjusted monthly to encourage trading around $100 par. And the weekly sale math comes out to basically $100 per share notional. That is the mechanism working almost exactly as intended, at scale.

Even more wild: Strategy’s STRC ATM program was sized at $4.2B, and after this filing it still had $1.9758B remaining. So the company has already used a bit over half that capacity, and this week showed it can still move massive size through the pipe. That is huge validation for liquidity, distribution, and investor appetite.

So the bullish read is simple:

STRC just proved it is not a side product.

It is the preferred security the market is absorbing in size, near par, with a fat monthly cash yield, while directly fueling Strategy’s bitcoin accumulation machine. That is why this looks insanely amazing for $STRC.

Want me to break down why this could also be insanely bullish for MSTR common as a second-order effect?